Some cool HOW TO WORK FROM HOME images:

There’s No Place Like Home

Image by *~Dawn~*

I’ve been trapped in the house working this weekend, and couldn’t get out today to enjoy the sunshine with my camera, so I took this pic of my yard through my kitchen window.

This pic goes out to one of my oldest flickr friends, Christian, who is the happiest person I know to be home right now. He returned home this weekend from Santiago, Chile, where he recently spent some of the worst days of his life. I’m so glad you’re safe and home now, my friend.

Thinking of how much "home" means when you’re far away from the ones you love made me appreciate being home this weekend, and feel blessed for what I have. You just never know when your life can change. Prayers & hope for the people of Chile.

I’m still working hard my friends, so am posting and running again. I can’t wait for things to slow down here so that I can spend some time on your streams seeing what you all have been up to.

Brooklyn Home Office, Minimized, At Night

Image by mkosut

I’ve spent the past few months figuring out how to scale down many of the things i don’t need and keeping my home office very minimal. That included ditching the large 30" apple cinema display (it blocked my view out the windows!) and going back to a simple laptop with two headless servers (on old G5 osx server pictured, and one ubuntu dual core 2.8ghz hp proliant server hidden behind the desk)

I’ve hidden my speakers behind the desk and stream via an airport express station to minimize cord plugins. The two cables visible below the desk have been hidden (ethernet for the osx server and some other cable) didn’t see them in the photo til it was too late.

I’ve purchased an all-in-one scanner/printer that fits comfortably in the sliding glass door cabinet for easy access.

My old and faithful aeron chair finally made it’s return home from vermont. Thank you for the gift adam, it’s lasted me years!

For white board drawings, i use dry erase markers on the glass windows. I make sure i don’t write any sensitive data on them as they’re clearly visible from the street ![]()

This provides maximum desk space to work with while not being distracted. i work from home occasionally (i’m a senior linux systems engineer for mtv networks/viacom) so i wanted someplace enjoyable to work without losing focus on my tasks.

I didn’t have any stones to put in the vase for the flower, so i ended up using all the silver change i could find. This works great because it looks interesting, but also makes it easy to ditch extra pocket change into it conveniently. No pennies allowed!

Pre-cleaning: www.flickr.com/photos/mkosut/2583927058/in/set-7215759430…

American Mailbox (Wakulla County, Florida) … Walk Away From Debt For a Better Future (March 24, 2011) …item 2.. FSU News – New school year, new resolutions — learn something exciting, and live life to the fullest. (Aug. 22, 2013)

Image by marsmet461

One time, my wife said to me, [imitating his wife] "Honey, the dryer is broken." [as himself] Did you check the lint trap? [imitating his wife with a clueless face] Sit down, honey, I’ll check it. [as his wife]

"Was there anything in there?" [as himself] Just a quilt. … Ron White … a/k/a Tater Salad.

.

…….*****All images are copyrighted by their respective authors ……..

.

……………………………………………………………………………………………………………………………………………………………………..

.

…..item 1a)…. The Huffingtonpost … HUFFPOST BUSINESS … Shifting the Focus From "Strategic Default" to "Prudent Walkaway"

Nicholas CarrollAuthor, "Walk Away From Debt for a Better Future"

Posted: March 24, 2011 07:38 PM

www.huffingtonpost.com/nicholas-carroll/shifting-the-focu…

A "strategic default" currently means walking away from an underwater home even though the owner could afford to pay the mortgage. However, this represents far less than half of walkaways. The vast majority of foreclosures happen to people who cannot afford to pay the mortgage.

Portrayals of strategic default in 2009 were typically of homeowners who "used their home as an ATM," or "deadbeats." Even news stories describing the positive side of default didn’t entirely shake those images. One of the earliest semi-positive stories was in the Wall St. Journal, titled "American Dream 2: Default, Then Rent." This article described a couple who had defaulted, cut their housing costs from nearly ,000/month to just over ,000/month, and were living in a bigger house with "a swimming pool with three waterfalls." Another strategic defaulter in the same article found the benefits of default-and-rent included the discretionary income to go out to dinner more often, and hang on to his series-6 BMW.

These are not the people I meet in the course of interviewing and writing about surviving tough times. The people I meet are laid off, or from two incomes down to one, or on their way to medical bankruptcy. They cannot imagine a swimming pool, much less a waterfall — they just have bills they can’t pay, one of which is the mortgage. Some are slow in adjusting to the "new normal," and still eat out regularly, but others have already cut back to eating out four times a year.

Their home may be underwater — or they may have equity. Often it doesn’t matter, when the bottom line is that they have to choose between the mortgage and medical insurance — because losing medical insurance in America is potentially lethal.

For this group, it is not a matter of cunningly defaulting to maintain a latte-sipping lifestyle. It is a matter of prudently walking away from the mortgage that is dragging their family and future under the waves.

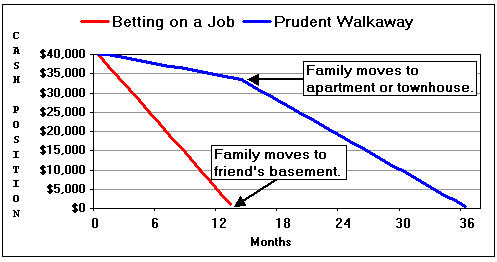

The benefit for people who act both prudently and decisively can be startling. Taking a fairly typical example from people I’ve interviewed, this is the family’s financial situation:

Primary income of ,000 net per month is gone, with one laid off.

Secondary income of ,000 net is still coming in.

,000 in cash and savings, including the 401K.

,000 in credit card debt.

One car fully paid for.

Second car — ,000 owed.

They have done a careful financial projection. The total monthly expenses are ,000, right down to the last dime — which includes ,500/month on mortgage and credit card bills. That says that if the main breadwinner is not fully employed in 14 months, they will lose the home — and of course take a dip in their credit rating. And if the job doesn’t come until the 13th month, it had better be at the same salary as the previous job, or they’ll lose the home anyway.

Scenario A: Betting on a job, and continuing to pay the mortgage (a.k.a. "doing the right thing," according to the moralists). They guess that they will be fully employed again in time to save the home. They continue paying mortgage, car payments, and minimum monthly credit card payments. If their bet is wrong, their trajectory is shown by the red line below.

Scenario B: Prudently walking away. They decide that getting a job might require a career shift or relocation, with some time and money invested in re-education. They immediately stop paying the mortgage and credit card payments. In this scenario, they cut their expenses by ,500/month (which rises to ,500/month when they move out and start paying rent). If there is real equity in their financed car, they sell it and buy a used car to replace it.

.

………………………………………………………..

Betting on a Job – Prudent Walkaway….

images.huffingtonpost.com/2011-03-22-prudenthomewalkaway.jpg

………………………………………………………..

.

………………………………………………………..

{kind=link}

Worksheet online in MS Excel format or PDF

www.walkawayfromdebt.com/worksheets&charts.html

.

……………………………………………………..

The difference between A and B is incredible. If the family bets the primary bread-winner will be working within the year and is wrong, they could be leaving their home without enough money to rent a decent apartment in 14 months — exhausted, frightened, and possibly running on bald tires. (People who "do the right thing" tend to leave long before they actually get legal notice to move.)

The family that bets the primary bread-winner will not find a job in 13 months and stops paying the debts will be leaving their home with ,000 cash in hand, move to a rental (usually in the same school district, if need be), and will have three years for the primary bread-winner to find a job. And that’s their worst scenario — it’s quite likely they’ll be in the house for 18-24 months without making any mortgage payments.

Conclusion: when the writing is on the wall, the best plan is often a prudent walkaway — an escape to the future, equipped with enough cash to get there.

.

.

.

………………………………………………………………………………………………………………………………………………………………………

.

…..item 1b)…. The Strategic Default Monitor …

Sunday, March 6, 2011

The 3 Must Send Debt Defense Letters

The 3 Must Send Letters

The following are the 3 "Must Send" Debt Defense letters. This means that at all times you must send any of these letters to any debt collection company or the original lender that contacts you

Read more »

Posted by Grinnin Skinny at 3:03 AM 2 comments

.

………………………………………………………

.

Monday, January 24, 2011

Consider Using A Mortgage Calculator, Amortization Table And Property Value Data For A Strategic Default

Part of our job at strategicdefault.org is to review other viewpoints about strategic default. This current post is inspired by another post we found while researching the universe of articles on strategic defaults and foreclosures.

We found this post entitled : “Should I Do a Strategic Default on my Mortgage?” by JLP in his blog All Financial Matters posted December 2, 2010.

This question was posed by a reader of JLP’s blog. The question and answer are as follows:

"I bought my condo at precisely the wrong time. I didn’t, however, listen to everyone telling me I could afford to buy more. I did a straight 30 year fixed that I could afford in reality. Of course I am incredibly underwater on my mortgage now. It is depressing, needless to say, and even more so when I feel as if my taxes are helping people who didn’t “do things the right way” and some companies who seemed to have contributed greatly to the problem and are not being held responsible…I live in Illinois, western burbs of Chicago…I bought for 9,000, now owe 2,000 and the most recent sale was ,000…30 year, 6.75% (which was good then!) percent…When I bought I planned on staying 5 years or so and moving up (didn’t everyone?). I don’t *need* to move. I sure wish I could buy some of the houses on the market now though! For what I paid? I bring home (after taxes) about ,000 a year. My mortgage + PMI + escrow is almost ,100…I know there are people in much worse shape. If I lost my job this whine about underwater wouldn’t even exist, you know? Still – just the though of paying even MORE out when I feel like I am not getting any benefit is upsetting, depressing."

The writer, JLP answers as follows:

Read more »

Posted by Grinnin Skinny at 12:06 AM 5 comments

Labels: a diji, amortization, augustine a diji, augustine ademola diji, augustine diji, ken mcallion, ken mccallion, kenneth mccallion, mortgage calculator, property value, strategic default

.

.

.

……………………………………………………………………………………………………………………………………………………………………….

.

…..item 1c)…. The Strategic Default Monitor … The 3 Must Send Debt Defense Letters …

Sunday, March 6, 2011

www.strategicdefault.org/2011/03/3-must-send-debt-defense…

.

.

.

………………………………………………………………………………………………………………………………………………………………………

.

…..item 2)…. New school year, new resolutions …

… FSU News … www.fsunews.com/ …

Aug. 22, 2013 12:35 PM |

Written by

Devyn Fussman

Contributing Writer

FILED UNDER

FSU News

FSU News Views

www.fsunews.com/article/20130822/FSVIEW03/130822013/New-s…

What do the first week in January and the last week in August have in common for Seminoles? New Year’s Resolutions. That special time of year when we start out with such good intentions, deluding ourselves into thinking that, if we come up with goals for ourselves to strive toward, we’ll somehow become better people. Then we realize we actually have to do these things, and they’re not always easy.

Usually, when we first start school, we figure that as long as we’re coming back with a clean slate, we might as well try to step up our game. In most cases we learn from the mistakes and procrastinations of last semester or last year, and strive to do better (I’d like to think that the reverse rarely happens). We think something like, “this year I’ll start my homework the day it’s assigned!” (insert laughter here); “this time I’ll make a special effort to go to class every day” (cue more laughter). Or, if you’re like most people, your goal is to be more organized in the new school year. According to a study published by the University of Scranton, this was number two in the top ten most popular resolutions (second to losing weight).

It all sounds good in theory, but most of the time people can’t even make it through the first two weeks without caving. Anyone else remember how crowded the Leach became in January, and how empty it was by March? Seventy-five percent of the people surveyed in the study who made resolutions were still at it after a week (meaning 25 percent can’t even keep it up that long), and after two weeks that number dropped to 71 percent, then down to 64 percent after one month and 46 percent after two months. The most discouraging statistic of all? Only eight percent were completely successful in sticking to their resolutions. Last year the FSView ran an article on how the first week of classes is nearly as stressful as finals week, because those are the only two weeks when everyone has to show up, whether they want to or not (not to mention the civil war that is the drop/add period). But it always seems to be the case that, after the crazy first week is over, we all go back to our old routines.

Despite this, most doctors and psychologists believe that Americans who make resolutions are ten times more likely to change their habits than those who don’t, just as long as those who do have a detailed and realistic game plan in mind. For example, you’ll probably have an easier time staying organized for classes if you set up a system before the first day. And hopefully after that first week, you’ll feel so good about yourself and so on top of the world that you’ll be more motivated to keep going.

Then, depending on your course load, you can tackle Top Ten Resolutions No. four and six: learn something exciting, and live life to the fullest.

.

.

.

……………………………………………………………………………………………………………………………………………………………………….

.

.

.

There's No Place Like Home

No comments:

Post a Comment